How you name a problem determines the solution space.

"Error handling" → logs, strings, retry buttons. "Trust repair" → copy, direction, safety. The reframe preceded everything

Users don't want to know how it works. Safe or not?

Technical explanations were skipped. "No money was deducted" outperformed paragraphs. Emotional safety first.

AARRR is only useful if you identify the right stage.

Calling this a Revenue problem misses it. Mapping it to Activation changed the investment case entirely.

A tight constraint produced a sharper idea.

Design only the recovery moment. That forced depth over breadth. Good scope is a creative decision.

ON SCOPE

ON FRAMING

ON USERS

ON STRATEGY

13 | WHAT I LEARNT

Not just about payments. About designing for trust.

Ready to buy.

Price accepted. Delivery fine

THINKING

FEELING

DOING

EMOTION

Confident.

Intent is clear

Reviews cart. Taps checkout.

High intent

UPI is fastest.

Always use this.

Routine.

Done this before.

Selects UPI. Enters PIN.

Peak confidence

Did my money leave? What happened? Should I try again?

Anxious. Confused.

Deduction fear is dominant.

Reads error. Checks bank app. Considers leaving.

Anxiety spike

Network issue. Not my fault. Card makes sense.

Reassured. Directed.

Product is still with me.

Reads recovery card. Taps Card.

Trust recovered

The Gap.

Product goes silent. This is the entire brief.

Recovery layer.

Explain. Direct. Restore.

01 | CART

02 | PAYMENT

03 | FAILURE

04 | RECOVERY

05 | JOURNEY MAP

What the user thinks, feels, and does at each step

Digital payments are a daily part of life, until they fail.

While success is seamless, failure isn’t just a technical event. It breaks trust, creates uncertainty, and leaves users guessing what to do next.

This project explores how payment systems can guide users through failure with clarity, reassurance, and adaptive suggestions reducing abandonment and restoring confidence.

Timeline

1 Week

My Team

Individual Project

My Role

UX Design

Interaction Prototyping

JavaScript Simulation

Visual Storytelling

Tools

Figma

FigJam

Miro

Visual Code

Designing for when Payments Fail

Reframing payment failure as a moment of trust repair

HYPOTHESIS I'M EXPLORING

When a payment fails, is the real problem the transaction or the uncertainty that follows?

01 | CONTEXT

What is this and where does this live?

The 30 seconds after a payment fails.

The most consequential, least designed moment in mobile commerce.

UPI: Bank-to-bank. NPCI. No card.

Card: Separate auth network. 3D Secure.

Wallet: Prepaid. Depletes silently.

Net banking: Bank portal. Session.

India processes 10B+ UPI transactions/month. Peak-hour failures exceed 20%. This is not an edge case. It's a primary case to design for.

→

→

→

→

Abandons

User decides alone.

"Payment Failed. Try Again."

Event Logged

Rail Fails

THE RAILS

WHY IT MATTERS

02 | PROBLEM

Success is designed. Failure is not.

Teams optimise for the happy path. Failure is an exception

In a multi-rail checkout in India that assumption is wrong.

"Payment Failed.

Try Again."

Technically accurate. Experientially, a dead end. No cause. No deduction status. No direction.

Silence. The product says nothing when it should speak.

Naked Recommendation. Alternatives without context read as commercial not helpful.

THE ASSUMPTION

THE CURRENT RESPONSE

THE TWO GAPS

Cart → Checkout

Tapped Pay

Rail Failed

Abandon after generic error

With recovery layer confirmed payments

The design problem

THE FAILURES ARE TECHNICAL. THE ABANDONMENT IS COMMUNICATIVE. ONLY ONE REQUIRES A DESIGN SOLUTION.

06 | FINDING THE LEAK

Where the funnel actually breaks

07 | THE CONCEPT

Four steps. In this order. Always.

01

Address the money first.

"No money was deducted." Before anything else. Dissolves the fear that causes abandonment.

02

Explain in plain English.

"Your UPI session timed out." Not the error code. Past tense - closed, not ongoing.

04

One CTA. No ambiguity.

Failed rail dims, not disappears. Dimming respects autonomy. Same infrastructure. Different 30 seconds.

03

Recommend with a reason.

"Card runs on a separate network." Context converts scepticism into action.

UPI failure rates of 30–55% are structurally normal in India. Network congestion, bank server downtime, VPA resolution failures, and UPI PIN timeouts are daily realities not edge cases. NPCI's own data shows peak-hour failures above 20% systemically.

Cards fail differently. 3DS authentication timeouts, insufficient balance false-positives, and international card routing errors account for most failures. These are resolvable but only if the UI tells the user what happened.

Wallets deplete silently. A failed wallet payment with no balance explanation causes confusion Explaining "Wallet balance: ₹0 remaining" unlocks a redirect to UPI.

The failure is technical. The abandonment is communicative. Users leave because e nothing told them what to do next.

Why do Indian payment rails fail at such high rates?

THE NEW MODEL

What does "trust architecture" mean in this context?

Trust architecture treats the failure moment as a designed experience, not a logged exception. It asks: what does the user need to know right now? What does the system know that the user doesn't? How do we translate technical failure into human direction?

The Recovery Layer is the implementation of this shift. It intercepts failure events and runs them through three layers: interpretation (what kind of failure is this?), communication (what should the user know?), and direction (what should the user do next?).

08| UI SCREENS

Every screen. Every decision.

FAILURE WARNING

A simple warning showing what happened when the transaction has failed.

RECOVERY INLINE ALERT

The users feel relief when they see a warning which gives them information rather than being left in the dark

RECOMMENDATION

Give an alternate method of transaction because the original mode of UPI Failed

01 - BASELINE

02 - PROCESSING

03 - FAILURE

04 - RECOVERY

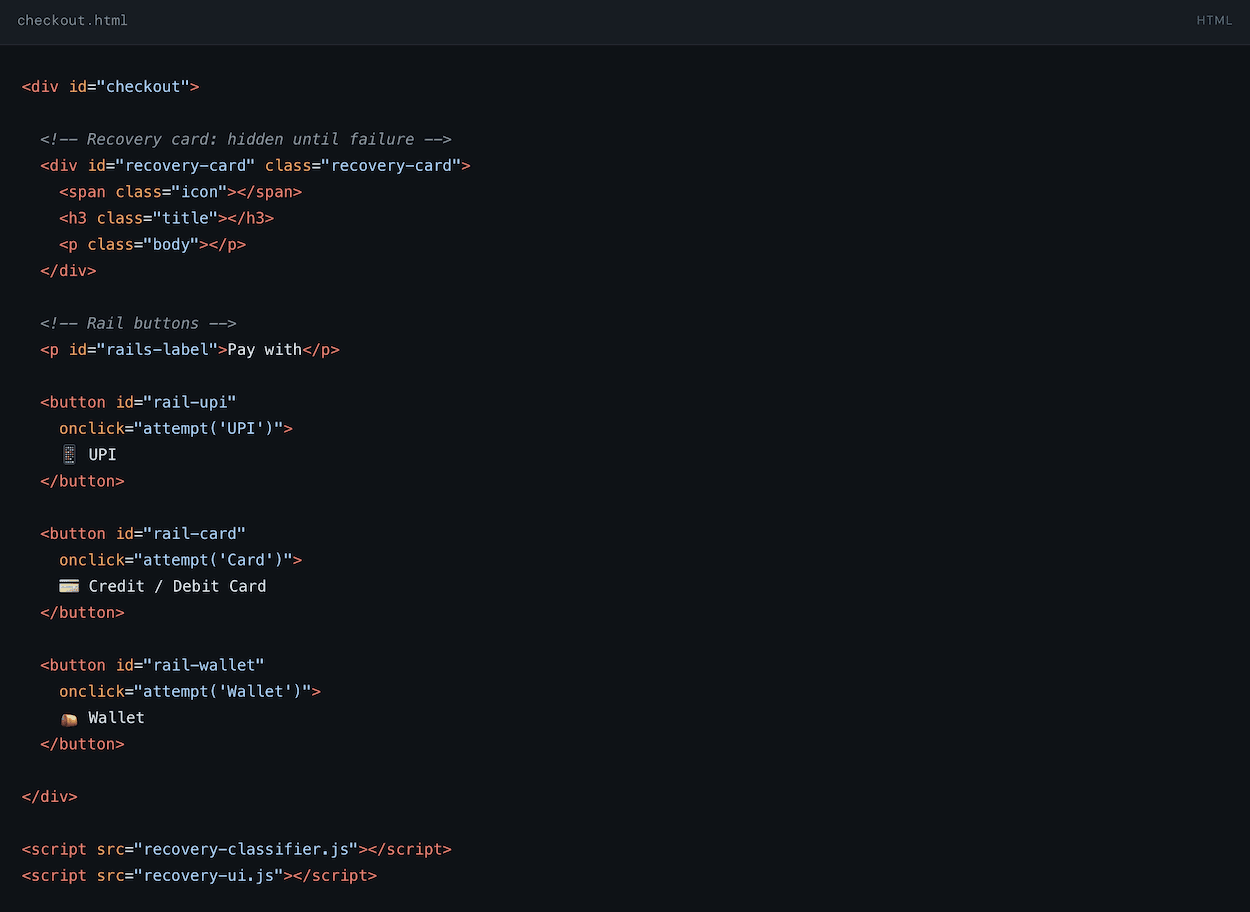

09 | THE CODE

How the recovery layer is actually implemented

FILE 1/3

The failure classifier - how does the system know what went wrong?

This is the brain. It maps rail + error code to a human-readable explanation. In production, the error code comes from your payment gateway response. In the prototype, failure is simulated with probability weights.

FILE 2/3

The UI renderer - how does the recovery state get painted to screen?

This function takes the classified failure object and updates the DOM. It shows the recovery card, dims the failed rail, and promotes the next best option to the top with a "Recommended" tag. No page reload required.

FILE 3/3

The HTML structure - what does the checkout markup look like?

This is the minimal HTML shell. The recovery card starts hidden. JS adds the visible class on failure. All rail buttons share the same ID pattern for the renderer to target them.

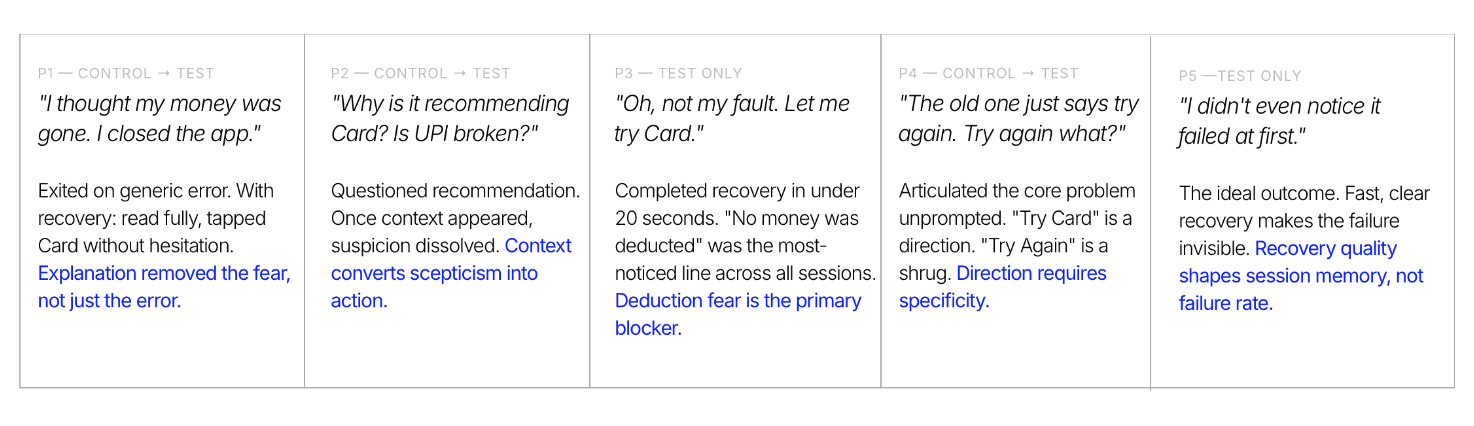

Exited on generic error. With recovery: read fully, tapped Card without hesitation. Explanation removed the fear, not just the error.

"I thought my money was gone. I closed the app."

Questioned recommendation. Once context appeared, suspicion dissolved. Context converts scepticism into action.

"Why is it recommending Card? Is UPI broken?"

Completed recovery in under 20 seconds. "No money was deducted" was the most-noticed line across all sessions. Deduction fear is the primary blocker.

"Oh, not my fault. Let me try Card."

Articulated the core problem unprompted. "Try Card" is a direction. "Try Again" is a shrug. Direction requires specificity.

"The old one just says try again. Try again what?"

The ideal outcome. Fast, clear recovery makes the failure invisible. Recovery quality shapes session memory, not failure rate.

"I didn't even notice it failed at first."

P1 — CONTROL → TEST

P2 — CONTROL → TEST

P3 — TEST ONLY

P4 — CONTROL → TEST

P5 —TEST ONLY

11 | USABILITY TESTING

5 participants.

Think-aloud. No lab.

Fear of deduction is the primary blocker, not the failure itself.

Why Harbour Molds Lines by Masterworks yet Sessions

Why Group Streamlining Onboarding and Saved With the Brightway

How Market.org Raisedup these RATE as 2x from Pathguide.

⸺ KEY FINDINGS

Razorpay or Cashfree sandbox API. Real error codes instead of simulated ones. One integration away from production-grade.

Connect to a real gateway sandbox.

Soon

Hypothesis: users who see the recovery layer have a higher 7-day return rate. That connects this directly to Retention with statistical confidence.

A/B test with 50+ users.

Later

12 | NEXT STEPS

Two moves. In this order.

Retry rate after failure

Context + direction produces willingness. Generic errors produce exits.

Post-failure abandonment

Guided recovery recaptures the majority before it becomes a lost conversion.

Early retention signal

Handled failure → trust deposit → return rate increase. The failure becomes a positive brand memory.

28%

−34%

↑Trust

10 | IMPACT

Recovery is a revenue lever

User arrives at checkout, intent present

Payment confirmed = first core value

Handled failure = trust deposit

Repeat purchase compounds from activation wins

"Their checkout worked when mine failed."

ACQUISITION

ACTIVATION

RETENTION

REVENUE

REFERRAL

SECONDARY

PRIMARY

ACTIVATION + RETENTION ARE WHERE PAYMENT RECOVERY CREATES VALUE. EVERYTHING ELSE COMPOUNDS FROM HERE.

03 | STRATEGY

Where this sits in the growth funnel

Glad we could cross paths!

I hope it left you with a bit of curiosity and inspiration.

LET'S CONNECT!

+91 96000 95584

→

→

→

→

Payment Confirmed

Processing

Tap Pay

Select Rail

Cart

→

→

→

Abandons

"Payment Failed. Try Again."

Processing

→

→

Alternative Rail Elevated.

Classified, Explained.

Processing

Confident Retry

SAME RAILS. SAME INFRASTRUCTURE. DIFFERENT 30 SECONDS

WITHOUT RECOVERY

WITH ADAPTIVE RECOVERY

No money deducted

Best rail surfaced

Payment confirmed

→

→

The right framework doesn't just measure the problem. It changes how seriously the team takes it.

Why Activation, not Revenue?

A failed payment is a failed activation the user never received core value. Teams that frame this as Revenue see a lost sale.

Teams that frame it as Activation see a failed first experiment. That reframe justifies design investment that pure revenue metrics never would.

Designing for when Payments Fail

Reframing payment failure as a moment of trust repair

Timeline

1 Week

My Role

UX Design

Interaction Prototyping

JavaScript Simulation

Visual Storytelling

My Team

Individual Project

Tools

Figma

FigJam

Miro

Visual Code

Digital payments are a daily part of life, until they fail.

While success is seamless, failure isn’t just a technical event. It breaks trust, creates uncertainty, and leaves users guessing what to do next.

This project explores how payment systems can guide users through failure with clarity, reassurance, and adaptive suggestions reducing abandonment and restoring confidence.

HYPOTHESIS I'M EXPLORING

When a payment fails, is the real problem the transaction or the uncertainty that follows?

India processes 10B+ UPI transactions/month. Peak-hour failures exceed 20%. This is not an edge case. It's a primary case to design for.

Rail Fails

↓

Event Logged

↓

"Payment Failed. Try Again."

↓

User decides alone.

↓

Abandons

02 | PROBLEM

Success is designed.

Failure is not.

THE ASSUMPTION

Teams optimise for the happy path. Failure is an exception

In a multi-rail checkout in India that assumption is wrong.

THE CURRENT RESPONSE

"Payment Failed.

Try Again."

Technically accurate. Experientially, a dead end. No cause. No deduction status. No direction.

THE TWO GAPS

Silence. The product says nothing when it should speak.

Naked Recommendation. Alternatives without context read as commercial not helpful.

01 | CONTEXT

What is this and where does this live?

The 30 seconds after a payment fails.

The most consequential, least designed moment in mobile commerce.

UPI: Bank-to-bank. NPCI. No card.

Card: Separate auth network. 3D Secure.

Wallet: Prepaid. Depletes silently.

Net banking: Bank portal. Session.

THE RAILS

WHY IT MATTERS

The right framework doesn't just measure the problem. It changes how seriously the team takes it.

Cart

↓

Select Rail

↓

Tap Pay

↓

Processing

↓

Payment Confirmed

04 | USER FLOW

The full path - including failure

Processing

↓

"Payment Failed. Try Again."

↓

Abandons

Processing

↓

Classified, Explained.

↓

Alternative Rail Elevated.

↓

Confident Retry

WITHOUT RECOVERY

↓

↓

05 | JOURNEY MAP

What the user thinks,

feels, and does at each step

Cart → Checkout

Tapped Pay

Rail Failed

Abandon after generic error

With recovery layer confirmed payments

The design problem

03

Recommend with a reason.

"Card runs on a separate network." Context converts scepticism into action.

04

One CTA. No ambiguity.

Failed rail dims, not disappears. Dimming respects autonomy. Same infrastructure. Different 30 seconds.

Why do Indian payment rails fail at such high rates?

UPI failure rates of 30–55% are structurally normal in India. Network congestion, bank server downtime, VPA resolution failures, and UPI PIN timeouts are daily realities not edge cases. NPCI's own data shows peak-hour failures above 20% systemically.

Cards fail differently. 3DS authentication timeouts, insufficient balance false-positives, and international card routing errors account for most failures. These are resolvable but only if the UI tells the user what happened.

Wallets deplete silently. Users don't track wallet balances. A failed wallet payment with no balance explanation causes confusion, not a retry. Explaining "Wallet balance: ₹0 remaining" immediately unlocks a redirect to UPI.

The failure is technical. The abandonment is communicative. Users don't leave because payment failed. They leave because nothing told them what to do next.

FILE 3/3

The HTML structure - what does the checkout markup look like?

This is the minimal HTML shell. The recovery card starts hidden. JS adds the visible class on failure. All rail buttons share the same ID pattern for the renderer to target them.

Retry rate after failure

Context + direction produces willingness. Generic errors produce exits.

28%

Post-failure abandonment

Guided recovery recaptures the majority before it becomes a lost conversion.

−34%

Early retention signal

Handled failure → trust deposit → return rate increase. The failure becomes a positive brand memory.

↑Trust

A/B test with 50+ users.

Later

How you name a problem determines the solution space.

"Error handling" → logs, strings, retry buttons. "Trust repair" → copy, direction, safety. The reframe preceded everything

Users don't want to know how it works. Safe or not?

Technical explanations were skipped. "No money was deducted" outperformed paragraphs. Emotional safety first.

AARRR is only useful if you identify the right stage.

Calling this a Revenue problem misses it. Mapping it to Activation changed the investment case entirely.

A tight constraint produced a sharper idea.

Design only the recovery moment. That forced depth over breadth. Good scope is a creative decision.

03 | STRATEGY

Where this sits in the growth funnel

User arrives at checkout, intent present

Payment confirmed = first core value

Handled failure = trust deposit

Repeat purchase compounds from activation wins

"Their checkout worked when mine failed."

ACQUISITION

ACTIVATION

RETENTION

REVENUE

REFERRAL

SECONDARY

PRIMARY

WITH ADAPTIVE RECOVERY

SAME RAILS. SAME INFRASTRUCTURE. DIFFERENT 30 SECONDS

06 | FINDING THE LEAK

Where the funnel actually breaks

07 | THE CONCEPT

Four steps. In this order. Always.

01

Address the money first.

"No money was deducted." Before anything else. Dissolves the fear that causes abandonment.

02

Explain in plain English.

"Your UPI session timed out." Not the error code. Past tense - closed, not ongoing.

THE NEW MODEL

What does "trust architecture" mean in this context?

Trust architecture treats the failure moment as a designed experience, not a logged exception. It asks: what does the user need to know right now? What does the system know that the user doesn't? How do we translate technical failure into human direction?

The Recovery Layer is the implementation of this shift. It intercepts failure events and runs them through three layers: interpretation (what kind of failure is this?), communication (what should the user know?), and direction (what should the user do next?).

08| UI SCREENS

Every screen.

Every decision.

09 | THE CODE

How the recovery layer is actually implemented

Three files. No framework required. Pure HTML, CSS, JavaScript. You can drop this into any existing checkout page. Here's what each piece does and why.

FILE 1/3

The failure classifier - how does the system know what went wrong?

This is the brain. It maps rail + error code to a human-readable explanation. In production, the error code comes from your payment gateway response. In the prototype, failure is simulated with probability weights.

FILE 2/3

The UI renderer - how does the recovery state get painted to screen?

This function takes the classified failure object and updates the DOM. It shows the recovery card, dims the failed rail, and promotes the next best option to the top with a "Recommended" tag. No page reload required.

10 | RECOVERY

Recovery is a revenue lever

11 | USABILITY TESTING

5 participants.

Think-aloud. No lab.

Phone in hand. Task given. Nothing explained. Half saw generic error first, then recovery. Half saw only recovery.

Fear of deduction is the primary blocker, not the failure itself.

Why Harbour Molds Lines by Masterworks yet Sessions

Why Group Streamlining Onboarding and Saved With the Brightway

How Market.org Raisedup these RATE as 2x from Pathguide.

Razorpay or Cashfree sandbox API. Real error codes instead of simulated ones. One integration away from production-grade.

Connect to a real gateway sandbox.

Soon

Hypothesis: users who see the recovery layer have a higher 7-day return rate. That connects this directly to Retention with statistical confidence.

13 | WHAT I LEARNT

Not just about payments.

About designing for trust.

12 | NEXT STEPS

Three moves.

In this order.

A simple warning showing what happened when the transaction has failed.

Give an alternate method of transaction because the original mode of UPI Failed

The users feel relief when they see a warning which gives them information rather than being left in the dark

ACTIVATION + RETENTION ARE WHERE PAYMENT RECOVERY CREATES VALUE. EVERYTHING ELSE COMPOUNDS FROM HERE.

A failed payment is a failed activation the user never received core value. Teams that frame this as Revenue see a lost sale.

Teams that frame it as Activation see a failed first experiment. That reframe justifies design investment that pure revenue metrics never would.

THE FAILURES ARE TECHNICAL. THE ABANDONMENT IS COMMUNICATIVE. ONLY ONE REQUIRES A DESIGN SOLUTION.

01 - BASELINE

02 - PROCESSING

03 - FAILURE

04 - RECOVERY

⸺ KEY FINDINGS

ON FRAMING

ON USERS

ON STRATEGY

ON SCOPE

Why Activation, not Revenue?

Glad we could cross paths!

I hope it left you with a bit of curiosity and inspiration.

LET'S CONNECT!

+91 96000 95584

FAILURE WARNING

RECOVERY INLINE ALERT

RECOMMENDATION

04 | USER FLOW

The full path - including failure